Denver Mayor Michael Hancock at State of the Cities 2020

Kathleen Lavine, Denver Business Journal

You may be telling yourself you’re going to wait to move – maybe you’re hoping mortgage rates will come down, prices will fall, or the market will feel a little easier.

And honestly? A lot of people feel that way right now. But here’s what some are starting to realize.

Waiting doesn’t usually fix the thing that made you want to move in the first place.

Your family still desperately needs more room. Your empty nest still feels too…empty.

Your parents or grandparents still need you to live closer.

You just got married… or divorced.

Your vision of retirement has you living somewhere else.

Eventually, life can reach a point where waiting feels harder than moving.

That’s why some people are still deciding to buy right now, even in today’s market. Not because conditions are perfect. But because the life changes behind their move never really went away.

And maybe that’s exactly where you are too. If so, you’re certainly not alone.

Data from the National Association of Realtors (NAR) shows 1 in 5 buyers last year said they felt like they had to purchase a home at that time, no matter the market.

That’s an important reminder right now. Sure, the dollars and cents of your move have to make sense for you. But big life changes happen whether mortgage rates and home prices are high, low, or somewhere in between.

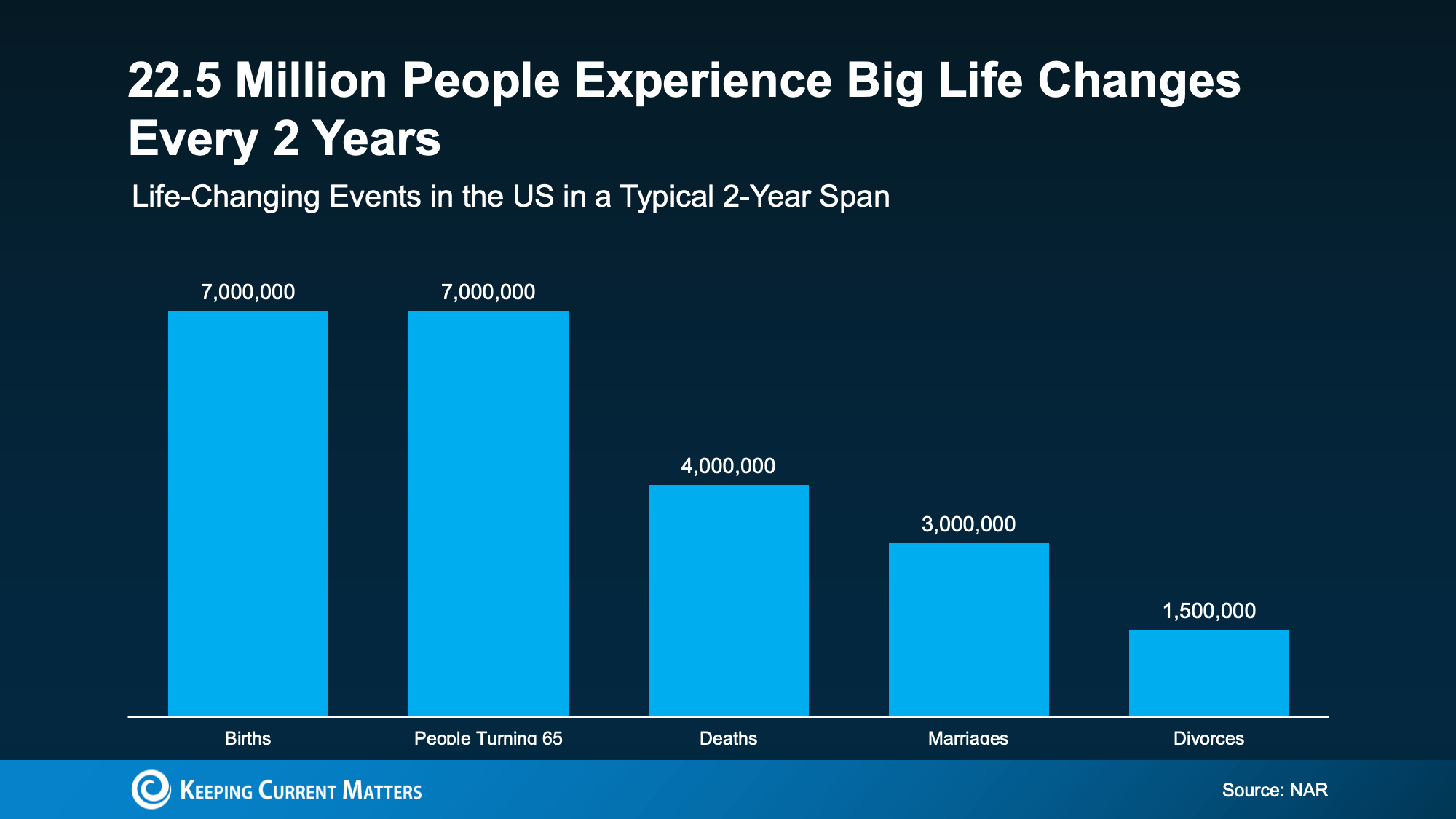

And those big life events happen more than you may think. NAR says roughly 22.5 million people experience major life changes in a typical two-year span (see graph below):

These are exactly the kinds of things that can change how much space you need, where you want to live, or what kind of lifestyle makes sense now. Chen Zhao, Head of Economics Research at Redfin, explains:

“Life doesn’t stand still—people get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood.”

And that’s what makes waiting so hard. Every month you spend hoping the market changes is another month living in a house that no longer works for your life. It’s stressful to feel stuck. And that feeling usually doesn’t disappear.

But while affordability is still a challenge, there may still be a way for you to make your move.

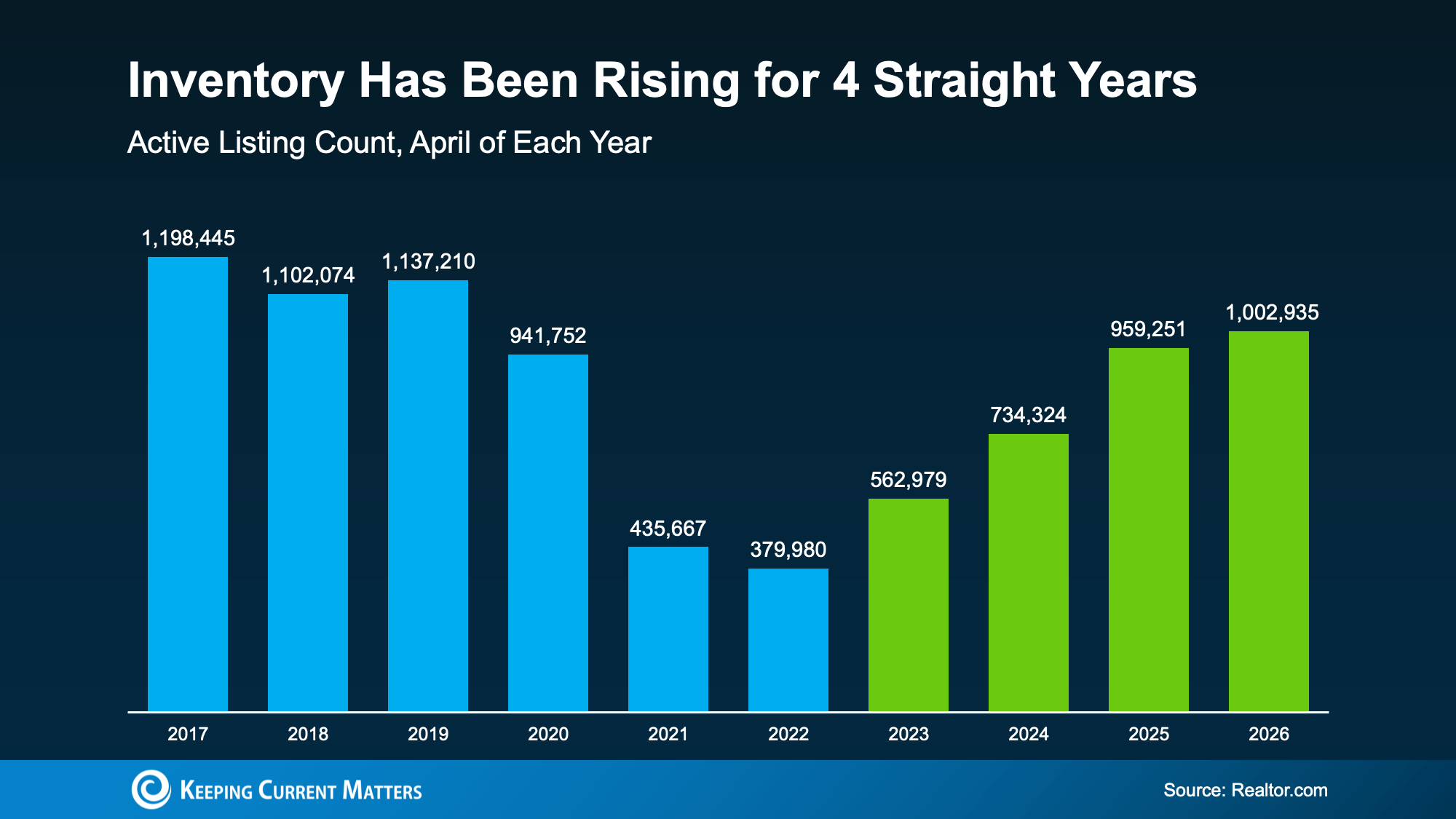

The number of homes for sale has been growing for 4 straight years (see graph below). That means more homes to choose from and, in some markets, more room to negotiate than buyers had just a few years ago.

That doesn’t mean moving is suddenly easy. But it does mean some buyers are finding ways to make a move work. So, if you’ve been putting your plans on hold, maybe the question isn’t just:

“What’s the market doing?” or “When will it get better?”

Maybe ask yourself this, too: “Can I still live where I’m at right now and make it work?”

If the answer to that second question is “no,” it may be worth having a conversation about what your options look like today – despite where rates or prices are. You could find your move is still possible after all. With more homes for sale, there’s a better chance to find one that fits your life (and your budget) right now.

Life changes. Priorities shift. Families grow. Kids move out. Careers evolve. And eventually, the house you’re in may stop fitting the life you’re living.

If that’s been weighing on you lately, talk to an agent about what your options could realistically look like today, no matter where rates or prices are.

Life can’t always wait for perfect market conditions. Maybe you don’t have to either.

Former Denver Mayor Michael Hancock is jumping into the real estate game.

Last week, Hancock completed what he hopes will be the first transaction building a portfolio of real estate holdings. He purchased the historic office building at 2413 N. Washington St. in Denver’s Five Points neighborhood, known as the Triangle Building.

Hancock bought the 7,600-square-foot building for just over $1.4 million, records show.

He served three terms as Denver’s mayor, from 2011 to 2023. Since then, Hancock has worked as a consultant, mostly in the realm of politics. Because the bulk of his career has been in the public sector, Hancock said it’s time for him to catch up financially, which he plans to do by investing in real estate.

“Real estate is still one of the more sure investments you can make,” Hancock said. “We’re going to continue to look and speculate and create opportunities with partners, and hopefully continue to expand. Once you get the bug and try to figure out how to do these things, the key would be to keep growing and hopefully amassing a nice portfolio.”

Starting with the 2413 N. Washington building made sense because Hancock already had a relationship with the previous owner.

He bought the property from the estate of Carl Bourgeois, a legendary Colorado developer known for his work to preserve and revitalize the historically Black area of Five Points. Bourgeois’ company, Civil Technology, also worked on the Denver International Airport, the Stapleton/Central Park Redevelopment Project, the Webb Municipal Office Building and the Denver Art Museum expansion, according to the company’s website.

Even before he was mayor, Hancock considered Bourgeois a friend, he said, calling Bourgeois someone he admired and who you couldn’t spend time in Five Points without knowing. Hancock grew up in the nearby Whittier neighborhood and said he spent a lot of his time there in his early twenties.

Michelle Glass, principal with Glass Properties Group at KW Commercial, represented Bourgeois’ daughters. She said Hancock was the ideal buyer because he won’t simply leave the building to flounder.

“What I was really looking for was to find an investor who was going to do something with the building,” Glass said. “In commercial real estate, especially with office, it’s definitely a buyer’s market, and we’re seeing a lot of vacant office space, as well as some vacant retail space in Five Points. So it was really exciting to be able to sell it to a buyer that is actually going to purchase that and do something with the building — reinvest in the building, renovate it.”

Glass, an experienced agent in the area, said it’s a great time to buy in Five Points because cap rates are high since building prices have been dampened since the Covid-19 pandemic.

“This will be a good thing for the community, because now new entrepreneurs and new investors can come in and do something and reuse some of these buildings,” she said. “To see the mayor come in and take a value-add building and reuse it for something that’s going to be profitable and great for the community is an exciting thing.”

Before Bourgeois bought the building in 1989, it had been used as an icehouse. He renovated it into office space.

Hancock now plans to renovate again, preserving historic elements while refreshing the space. He plans to lease several office suites and add co-working space, a cafe and a garden area so people can work outside.

“We plan to program it as well to have maybe some discussions, speak easy-type activity with guest speakers and things of that nature,” Hancock said.

He is determining what the renovation will cost, Hancock said. He and his fiancée are the majority owners of the property, and they have three silent partners, he said.

Part of the deal included seller financing, Glass said, which helped make the sale more favorable for both parties.

For Hancock, Five Points is a target area as he continues his real estate career.

“It’s an important area,” he said. “It has been gentrified. We want to create some ownership down there again and continue to create diversity and opportunities for everyone down there. I want to be a part of that. …Five Points is burning to continue to get better.”

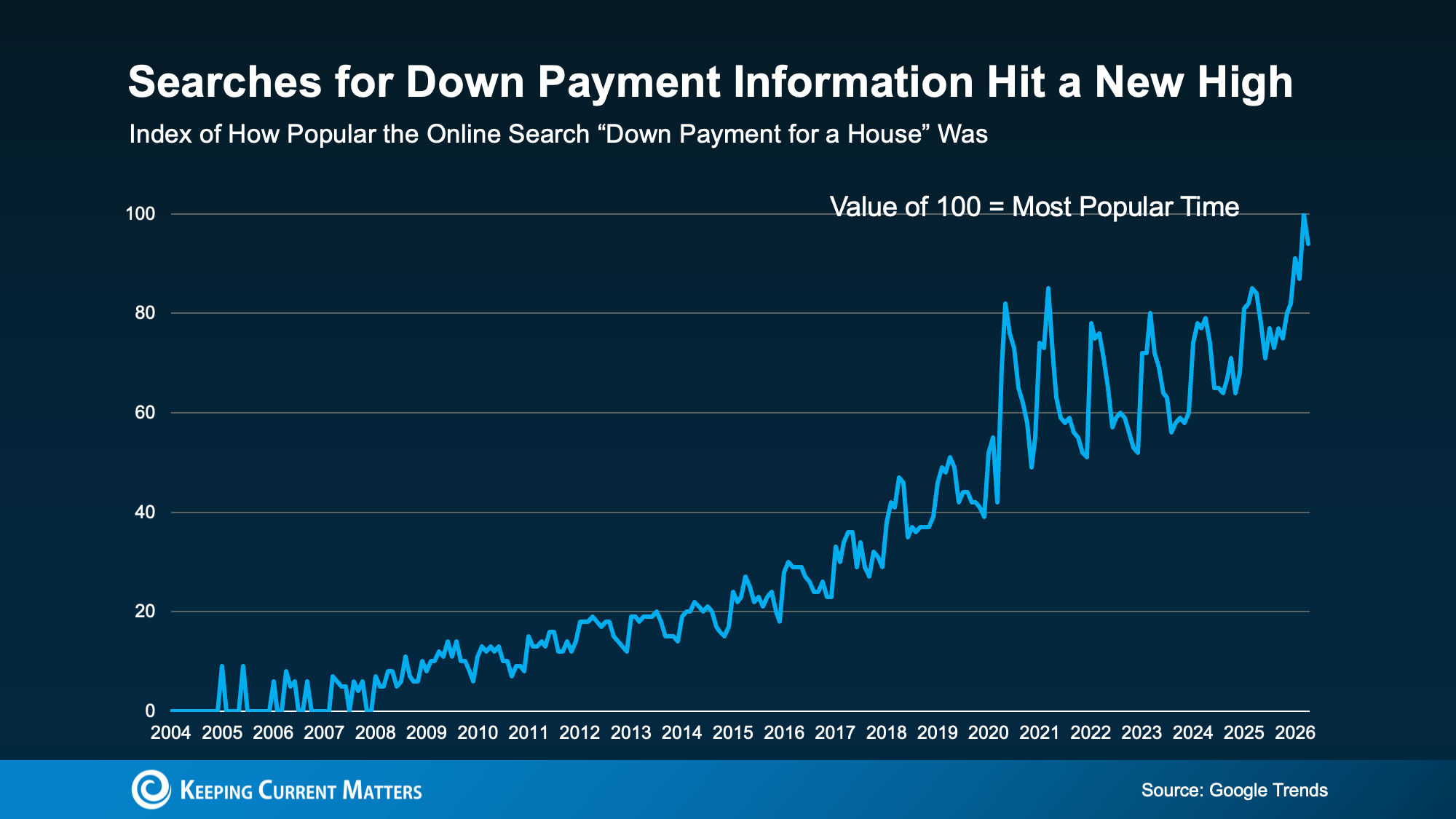

According to Google Trends, online searches for down payment information recently hit an all-time high. And that’s a clear sign more buyers are trying to figure out what they really need to save before making a move (see graph below):

If you’re wondering the same thing, you can always turn to the internet for answers. But a lot of the time, it’s better to ask a local expert. Because here’s what a pro would tell you.

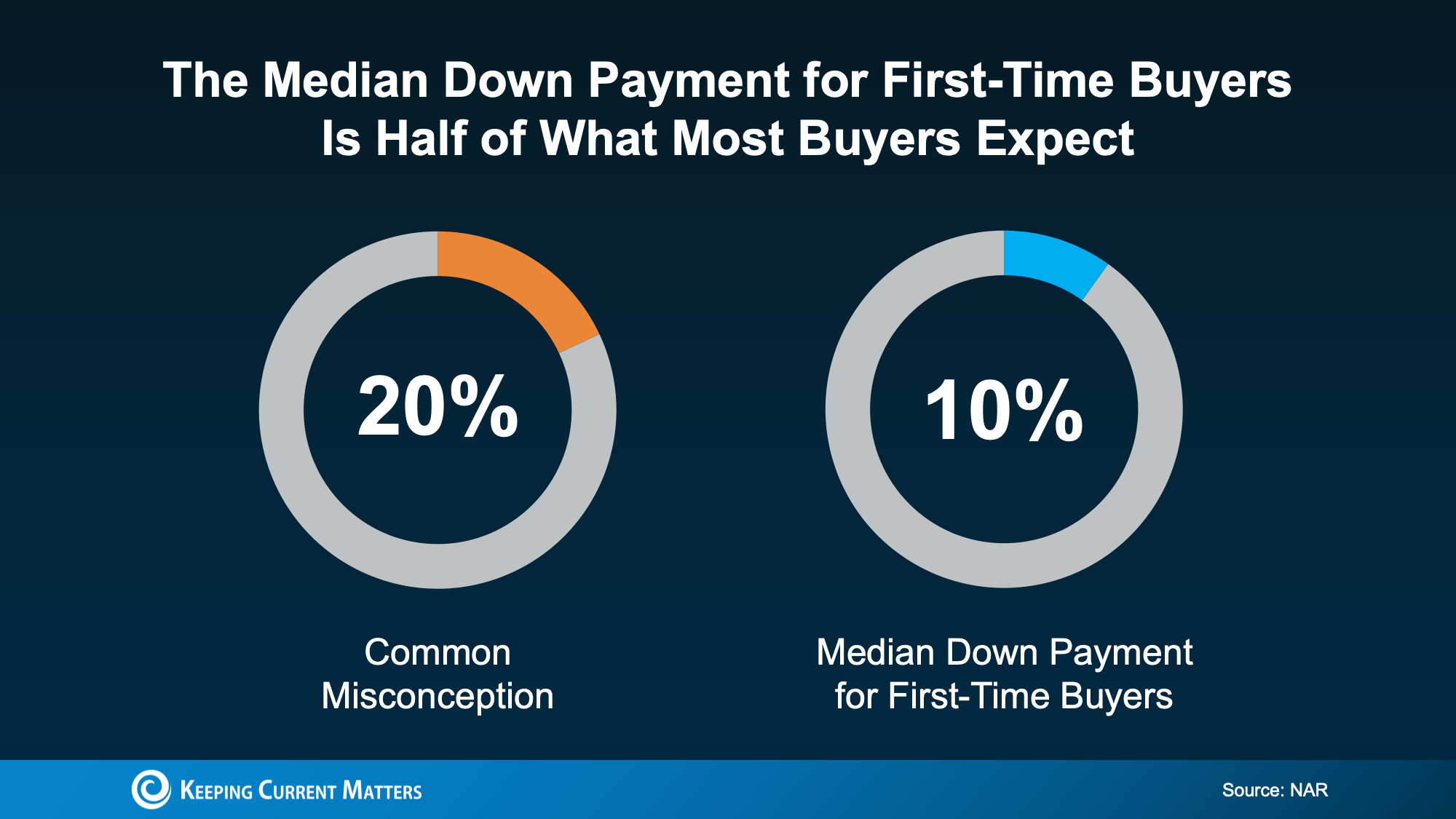

The idea that you need 20% down to buy a home is one of the biggest misconceptions around the homebuying process. And the data debunks the myth.

While there are benefits to putting that much money down, most first-time buyers put down far less.

Here’s why. Unless it’s stated by your lender, you typically don’t have to have a 20% down payment. There are even some loan options designed to help you get into a home with a much smaller upfront cost. As the Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available, and you don’t need to put down the traditional 20% . . . many homebuyers are able to secure a home with as little as 3% or even no down payment at all . . .”

For example, FHA loans allow down payments as low as 3.5%, while VA and USDA loans offer zero down payment options for qualified applicants, like Veterans.

And those options are just one reason so many first-time buyers are able to buy without a 20% down payment.

So, if buyers aren’t doing 20%, how much do they actually put down?

According to the National Association of Realtors (NAR), the median down payment for first-time homebuyers is only 10%. That’s half of what you probably expected.

That means if you’re aiming to save 20% because you think you have to, you may be setting a timeline that’s longer than necessary.

And here’s some more good news. It’s not only that you may be able to buy with less money down than you thought, but there are also options to help you get to your down payment goal even faster.

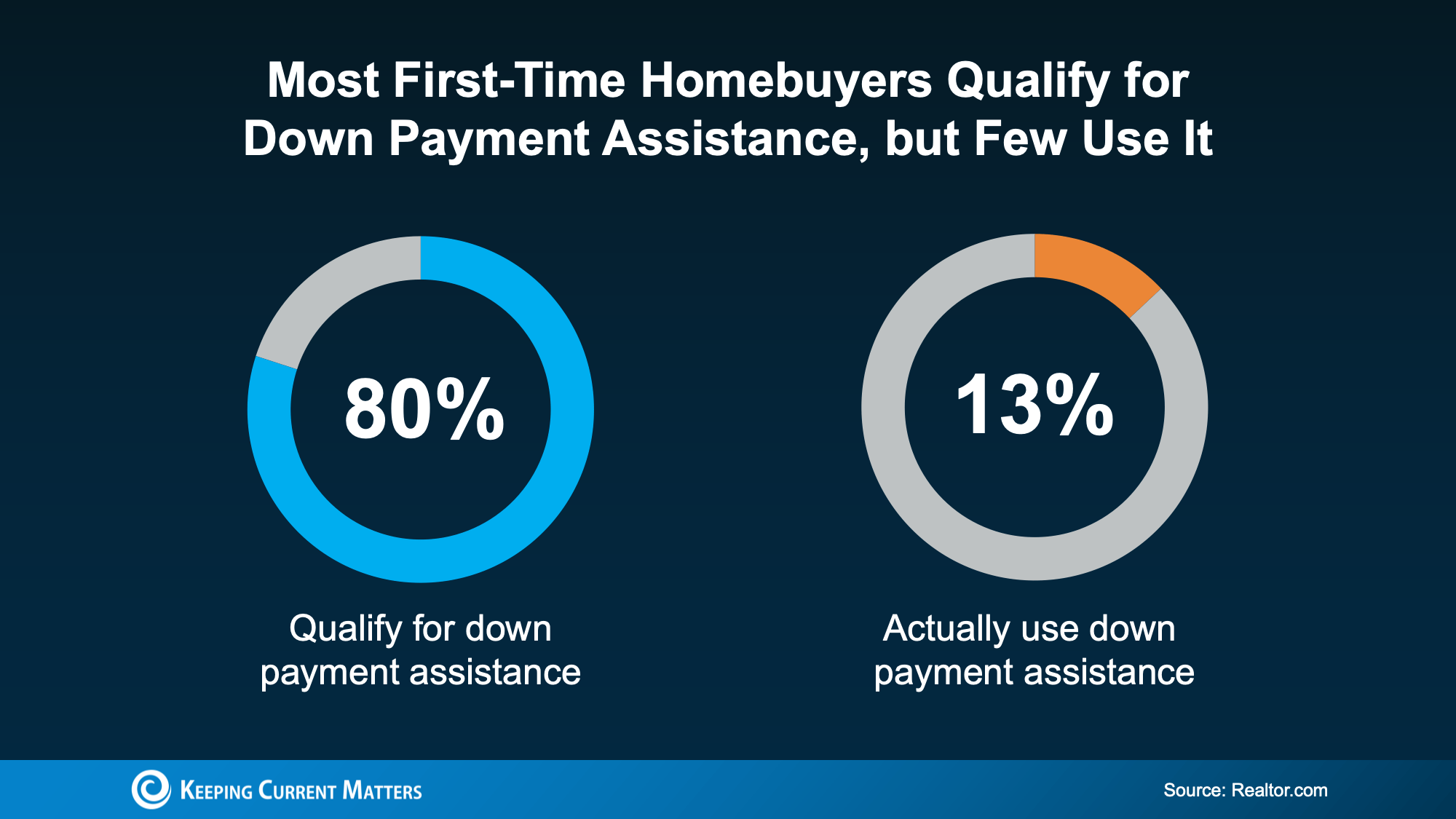

There are a lot of programs designed to help you save for a down payment – and they can make a big difference in how fast you hit your savings target. Unfortunately, buyers don’t realize how many there are, or that they may qualify for help.

Research from Realtor.com shows almost 80% of first-time homebuyers qualify for down payment assistance (DPA), but only 13% actually use it (see chart below):

And that’s another big miss holding would-be buyers like you back.

In the U.S., there are over 2,600 homeownership programs available, many offering significant financial support. As Down Payment Resource shares:

“With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.”

Imagine how much further your savings could go with an extra $18,000 you can use to buy. In some cases, you may even be able to stack multiple programs, giving what you’ve saved an even bigger boost.

The simple truth is: most first-time buyers don’t put 20% down. And if you’ve been waiting to buy until you have that saved, you may be setting a timeline that’s longer than necessary.

To find out what you really need to save and if you qualify for any help, connect with a trusted lender who can walk you through your options. You may be able to buy sooner than you thought.